The Inventory That Continually Discloses the Amount of Inventory on Hand is Called

Notes of Financial & Managerial Accounting

8 Inventories and the Cost of Goods Sold

INVENTORY DEFINED

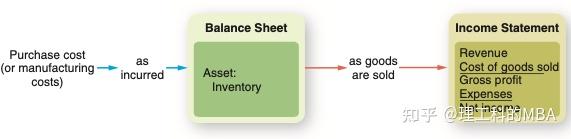

In a merchandising company, inventory consists of all goods owned and held for sale to customers. Inventory is expected to be converted into cash within the company's *operating cycle.*1 In the balance sheet, inventory is listed immediately after accounts receivable, because it is just one step farther removed from conversion into cash than customer receivables.

8.1 The Flow of Inventory Cost

Inventory is a nonfinancial asset and usually is shown in the balance sheet at its cost. As items are sold from inventory, their costs are removed from the balance sheet and transferred to the cost of goods sold, which is offset against sales revenue in the income statement.

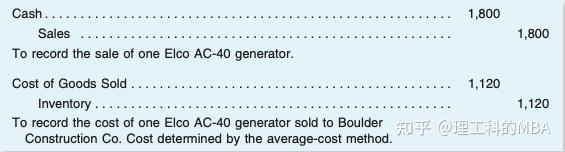

In a perpetual inventory system, entries in the accounting records parallel this flow of costs. When merchandise is purchased, its cost (net of allowable cash discounts) is added to the asset account Inventory. As the merchandise is sold, its cost is removed from the Inventory account and transferred to the Cost of Goods Sold account.

The valuation of inventory and cost of goods sold is of critical importance to managers and to external users of financial statements. In many cases, inventory is a company's largest asset, and the cost of goods sold is its largest expense. These two accounts have a significant effect on the financial statement subtotals and ratios used in evaluating the liquidity and profitability of the business.

WHICH UNIT DID WE SELL?

Purchases of merchandise are recorded in the same manner under all of the inventory valuation methods. The differences in these methods lie in determining which costs should be removed from the Inventory account when merchandise is sold.

In practice, a company often has in its inventory identical units of a given product that were acquired at different costs. Acquisition costs may vary because the units were purchased at different dates, from different suppliers, or in different quantities.

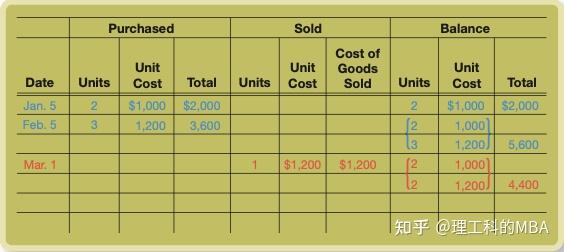

DATA FOR ALL ILLUSTRATION

A new cost layer is created whenever units are acquired at a different per-unit cost.

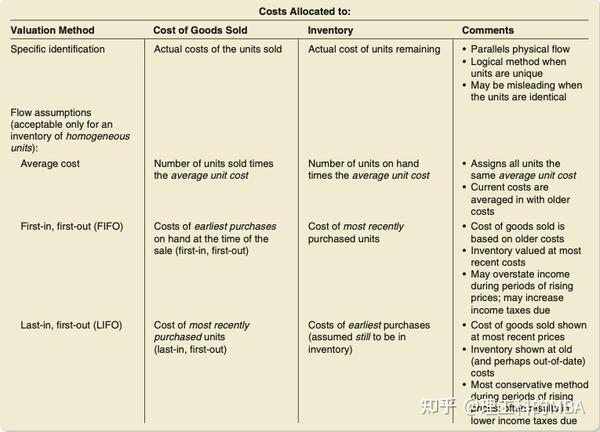

SPECIFIC IDENTIFICATION

The specific identification method can be used only when the actual costs of individual units of merchandise can be determined from the accounting records. The actual cost of this particular unit then is used in recording the cost of goods sold.

COST FLOW ASSUMPTIONS

Using a cost flow assumption, often referred to as simply a flow assumption, is particularly common where the company has a large number of identical inventory items that were purchased at different prices.

When a cost flow assumption is in use, the seller makes an assumption as to the sequence in which units are withdrawn from inventory.

Three cost flow assumptions are in widespread use:

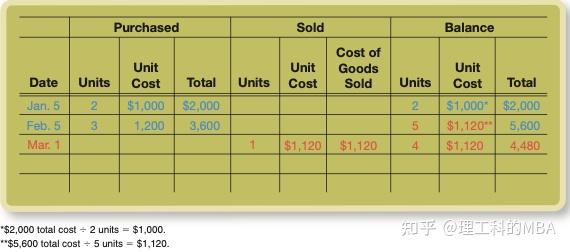

- Average cost. This assumption values all merchandise—units sold and units remaining in inventory—at the average per-unit cost. (In effect, the average-cost method assumes that units are withdrawn from the inventory in random order.)

- First-in, first-out (FIFO). As the name implies, FIFO involves the assumption that goods sold are the first units that were purchased—that is, the oldest goods on hand. Thus the remaining inventory is comprised of the most recent purchases.

- Last-in, first-out (LIFO). Under LIFO, the units sold are assumed to be those most recently acquired. The remaining inventory, therefore, is assumed to consist of the earliest pur- chases.

The cost flow assumption selected by a company need not correspond to the actual physical movement of the company's merchandise. When the units of merchandise are identical (or nearly identical), it does not matter which units are delivered to the customer in a particular sales transaction. Therefore, in measuring the income of a business that sells units of identical merchandise, accountants consider the flow of costs to be more important than the physical flow of the merchandise.

The use of a cost flow assumption eliminates the need for separately identifying each unit sold and looking up its actual cost. Experience has shown that these cost flow assumptions provide useful and reliable measurements of the cost of goods sold, as long as they are applied consistently to all sales of the particular type of merchandise.

AVERAGE-COST METHOD

When the average-cost method is in use, the average cost of all units in inventory is com- puted after every purchase. This average cost is computed by dividing the total cost of goods available for sale by the number of units in inventory. Because the average cost may change following each purchase, this method also is called the moving average method when a perpetual inventory system is used.

Notice that the Unit Cost column for purchases still shows actual unit costs. The Unit Cost columns relating to sales and to the remaining inventory, however, show the average unit cost.

Under the average-cost assumption, all items in inventory are assigned the same per-unit cost (the average cost). Hence, it does not matter which units are sold; the cost of goods sold always is based on the current average unit cost.

FIRST-IN, FIRST-OUT METHOD

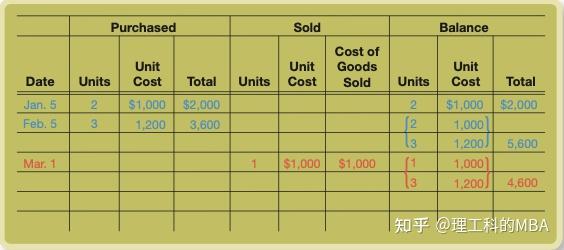

The first-in, first-out method, often called FIFO, is based on the assumption that the first merchandise purchased is the first merchandise sold.

Notice that FIFO uses actual purchase costs, rather than an average cost. Thus, if merchandise has been purchased at several different costs, the inventory will include several different cost layers. The cost of goods sold for a given sales transaction also may involve several different cost layers.

As the cost of goods sold always is recorded at the oldest available purchase costs, the units remaining in inventory are valued at the more recent acquisition costs.

LAST-IN, FIRST-OUT METHOD

The last-in, first-out method, commonly known as LIFO, is among the most widely used methods of determining the cost of goods sold and valuing inventory. As the name suggests, the most recently purchased merchandise (the last in) is assumed to be sold first.

Like FIFO, the LIFO method uses actual purchase costs, rather than an average cost. Thus, the inventory may have several different cost layers. If a sale includes more units than are included in the most recent cost layer, some of the goods sold are assumed to come from the next most recent layer.

As LIFO transfers the most recent purchase costs to the cost of goods sold, the goods remaining in inventory are valued at the oldest acquisition costs.

EVALUATION OF THE METHODS

All three of the cost flow assumptions just described are acceptable for use in financial statements and in income tax returns.

The only requirement for using a flow assumption is that the units to which the assumption is applied should be homogeneous in nature—that is, virtually identical to one another. If each unit is unique, such as the sale of portraits by an art studio, only the specific identification method can properly match sales revenue with the cost of goods sold.

However, the method (or methods) used in financial statements always should be disclosed in notes accom- panying the statements.

Specific Identification

The specific identification method is best suited to inven- tories of high-priced, low-volume items.

However, when the units in inventory are identical (or nearly identical), the specific identification method may produce misleading results by implying differences in value that—under current market conditions—do not exist. There is also the potential to manipulate the company's financial statement numbers by selecting which items (and as a result which costs) are sold.

Average Cost

Identical items will have the same accounting values only under the average-cost method. It is not necessary to keep track of the specific items sold and of those still in inventory. Also, it is not possible to manipulate income merely by selecting the specific items to be delivered to customers.

A shortcoming of the average-cost method is that changes in current replacement costs of inventory are concealed because these costs are averaged with older costs. Thus neither the valuation of ending inventory nor the cost of goods sold will quickly reflect changes in the current replacement cost of merchandise.

First-In, First-Out

The distinguishing characteristic of the FIFO method is that the oldest purchase costs are transferred to the cost of goods sold, while the most recent costs remain in inventory.

When purchase costs are rising, the FIFO method assigns lower (older) costs to the cost of goods sold and the higher (more recent) costs to the goods remaining in inventory.

By assigning lower costs to the cost of goods sold, FIFO usually causes a business to report higher profits than would be reported under the other inventory valuation methods. Some companies favor the FIFO method for financial reporting purposes, because their goal is to report the highest net income possible. For income tax purposes, however, reporting more income than necessary results in paying more income taxes than necessary.

Some accountants and decision makers believe that FIFO tends to overstate a company's profitability in periods of rising prices. Revenue is based on current market conditions. By offsetting this revenue with a cost of goods sold based on older (and lower) prices, gross profits may be overstated consistently.

A conceptual advantage of the FIFO method is that in the balance sheet inventory is valued at recent purchase costs. Therefore, this asset appears in the balance sheet at an amount more closely approximating its current replacement cost.

Last-In, First-Out

The basic assumption in the LIFO method is that the most recently purchased units are sold first and that the older units remain in inventory.

For the purpose of measuring income, most accountants consider the flow of costs more important than the physical flow of merchandise. Supporters of the LIFO method contend that the measurement of income should be based on current market conditions. Therefore, current sales revenue should be offset by the current cost of the merchandise sold. By the LIFO method, the costs assigned to the cost of goods sold are relatively current because they reflect the most recent purchases.

There is one significant shortcoming to the LIFO method. The valuation of the asset inventory is based on the company's oldest inventory acquisition costs. After the company has been in business for many years, these oldest costs may greatly understate the current replacement cost of the inventory. Thus, when an inventory is valued by the LIFO method, the company also should disclose the current replacement cost of the inventory in a note to the financial statements.

During periods of rising inventory replacement costs, the LIFO method results in the lowest valuation of inventory and measurement of net income. Therefore, LIFO is regarded as the most conservative of the inventory pricing methods. FIFO, on the other hand, is the least conservative method.

Income tax considerations are the principal strategic reason for the popularity of the LIFO method. Remember that the LIFO method assigns the most recent inventory purchase costs to the cost of goods sold. In the common situation of rising prices, these most recent costs are also the highest costs. By reporting a higher cost of goods sold than results from other inventory valuation methods, the LIFO method usually results in lower taxable income. In short, if inventory costs are rising, a company can reduce the amount of its income tax obligation by using the LIFO method in its income tax return.

It may seem reasonable that a company would use the LIFO method in its tax return to reduce taxable income and use the FIFO method in its financial statements to increase the amount of net income reported to investors and creditors. However, income tax regulations allow a corporation to use LIFO in its income tax return only if the company also uses LIFO in its financial statements. Thus, income tax considerations often provide the overriding strategic reason for selecting the LIFO method.

DO INVENTORY METHODS REALLY AFFECT PERFORMANCE?

Except for their effects on income taxes, the answer to this question is no.

During a period of rising prices, a company might report higher profits by using FIFO instead of LIFO. But the company would not really be any more profitable. An inventory valuation method affects only the allocation of costs between the Inventory account and the Cost of Goods Sold account. It has no effect on the total costs actually incurred in purchasing or manufacturing inventory. Except for the amount of income taxes paid, differences in the profitability reported under different inventory methods exist only on paper.

The inventory method in use does affect the amount of income taxes owed. To the extent that an inventory method reduces these taxes, it does increase profitability.

THE PRINCIPLE OF CONSISTENCY

The principle of consistency is one of the basic concepts underlying reliable financial state- ments. This principle means that, once a company has adopted a particular accounting method, it must follow that method consistently, rather than switch methods from one year to the next. Thus, once a company has adopted a particular inventory flow assumption (or the specific identification method), it should continue to apply that assumption to all sales of that type of merchandise.

The principle of consistency does not prohibit a company from ever changing its account- ing methods. If a change is made, however, the reasons for the change must be explained, and the effects of the change on the company's net income must be fully disclosed.

JUST-IN-TIME (JIT) INVENTORY SYSTEMS

The phrase "just-in-time" usually means that purchases of raw materials and component parts arrive just in time for use in the manufacturing process—often within a few hours of the time they are scheduled for use. A second application of the just-in-time concept is completing the manufacturing process just in time to ship the finished goods to customers.

The concept of minimizing inventories applies more to manufacturing operations than to retailers.

The just-in-time concept actually involves much more than minimizing the size of inven- tories. It has been described as the philosophy of constantly working to increase efficiency throughout the organization. One basic goal of an accounting system is to provide management with useful information about the efficiency—or inefficiency—of operations.

8.2 Taking a Physical Inventory

The primary reason for this procedure of "taking inventory" is to adjust the perpetual inventory records for unrecorded shrinkage losses, such as theft, spoilage, or breakage.

The physical inventory usually is taken at (or near) the end of the company's fiscal year. Often a business selects a fiscal year ending after a period of high activity.

RECORDING SHRINKAGE LOSSES

In most cases, the year-end physical count of the inventory reveals some shortages or damaged merchandise. The costs of missing or damaged units are removed from the inventory records using the same flow assumption as is used in recording the costs of goods sold.

The inventory flow assumption in use affects the measurement of shrinkage losses in the same way it affects the cost of goods sold. If the company uses FIFO, for example, the missing units will be valued at the oldest purchase costs shown in the inventory records. But if this company uses LIFO, the missing units all will be assumed to have come from the most recent purchase.

If shrinkage losses are small, the costs removed from inventory may be charged (debited) directly to the Cost of Goods Sold account. If these losses are material in amount, the offsetting debit should be entered in a special loss account, such as Inventory Shrinkage Losses. In the income statement, a loss account is deducted from revenue in the same manner as an expense account.

LCM AND OTHER WRITE-DOWNS OF INVENTORY

In addition to shrinkage losses, the value of inventory may decline because the merchandise has become obsolete or is unsalable for other reasons. If inventory has become obsolete or is otherwise unsalable, its carrying amount in the accounting records should be written down to zero (or to its "scrap value," if any). A write-down of inventory reduces both the carrying amount of the inventory in the balance sheet and the net income of the current period. The reduction in income is handled in the same manner as a shrinkage loss. If the write-down is relatively small, the loss is debited directly to the Cost of Goods Sold account. If the write- down is material in amount, however, it is charged to a special loss account, perhaps entitled Loss from Write-Down of Inventory.

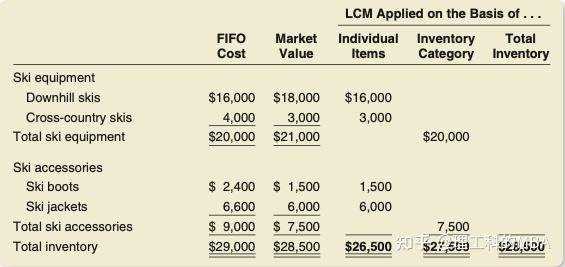

The Lower-of-Cost-or-Market (LCM) Rule

An asset is an economic resource. It may be argued that no economic resource is worth more than it would cost to replace that resource in the open market. For this reason, accountants traditionally have valued inventory in the balance sheet at the lower of its (1) cost or (2) market value. In this context, "market value" usually means current replacement cost. Thus the inventory is valued at the lower of its historical cost or its current replacement cost. This accounting convention is referred to as the lower-of-cost-or-market (LCM) rule.

The LCM rule can be used in conjunction with any cost flow assumption. It may also be applied on the basis of individual inventory items, major inventory categories, or the entire inventory. To illustrate, assume that Joel's Ski Shop uses the FIFO cost flow assumption.

In their financial statements, most companies state that inventory is valued at the lower-of-cost-or-market. In an inflationary economy, however, the lower of these two amounts is usually cost, especially for companies using LIFO.

THE YEAR-END CUTOFF OF TRANSACTIONS

A proper cutoff simply means that the transactions occurring near year-end are recorded in the correct accounting period.

One aspect of a proper cutoff is determining that all purchases of merchandise through the end of the period are recorded in the inventory records and included in the physical count of merchandise on hand at year-end. Of equal importance is determining that the cost of all merchandise sold through the end of the period has been removed from the inventory accounts and charged to the Cost of Goods Sold. This merchandise should not be included in the year- end physical count.

If some sales transactions have not been recorded as of year-end, the quantities of merchandise shown in the inventory records will exceed the quantities actually on hand. When the results of the physical count are compared with the inventory records, these unrecorded sales easily could be mistaken for inventory shortages.

Making a proper cutoff may be difficult if sales transactions are occurring while the merchandise is being counted. For this reason, many businesses count their physical inventory during nonbusiness hours, even if they must shut down their sales operations for a day.

Matching Revenue and the Cost of Goods Sold

Accountants must determine that both the sales revenue and the cost of goods sold relating to sales transactions occurring near year-end are recorded in the same accounting period. Otherwise, the revenues and expenses from these transactions will not be properly matched in the company's income statements.

Goods in Transit

A sale should be recorded when title to the merchandise passes to the buyer. If these terms are F.O.B. (free on board) shipping point, title passes at the point of shipment and the goods are the property of the buyer while in transit. If the terms of the shipment are F.O.B. destination, title does not pass until the shipment reaches its destination and the goods belong to the seller while in transit.

It usually is most convenient to record all purchases when the inbound shipments arrive and all sales when the merchandise is shipped to the customer.

PERIODIC INVENTORY SYSTEMS

In a periodic inventory system, the cost of merchandise purchased during the year is debited to a Purchases account, rather than to the Inventory account. When merchandise is sold to a customer, an entry is made recognizing the sales revenue, but no entry is made to reduce the inventory account or to recognize the cost of goods sold.

The inventory on hand and the cost of goods sold for the year are not determined until year-end. At the end of the year, all goods on hand are counted and priced at cost. The cost assigned to this ending inventory is then used to compute the cost of goods sold.

The only item in this computation that is kept continuously up-to-date in the accounting records is the Purchases account. The amounts of inventory at the beginning and end of the year are determined by annual physical observation.

Determining the cost of the year-end inventory involves two distinct steps: counting the merchandise and pricing the inventory—that is, determining the cost of the units on hand. Together, these procedures determine the proper valuation of inventory and the cost of goods sold.

Applying Flow Assumptions in a Periodic System

In our discussion of per- petual inventory systems, we have emphasized the costs that are transferred from inventory to the cost of goods sold as the sales occur. In a periodic system, the emphasis shifts to determin- ing the costs that should be assigned to inventory at the end of the period.

Specific Identification

The cost of goods sold then is determined by subtracting this ending inventory from the cost of goods available for sale.

Average Cost

The average cost is determined by dividing the total cost of goods available for sale during the year by the total number of units available for sale.

FIFO

Under the FIFO flow assumption, the oldest units are assumed to be the first sold. The ending inventory, therefore, is assumed to consist of the most recently acquired goods. (Remember, we are now talking about the goods remaining in inventory, not the goods sold.)

Notice that the FIFO method results in an inventory valued at relatively recent purchase costs. The cost of goods sold, however, is based on the older acquisition costs.

LIFO

Under LIFO, the last units purchased are considered to be the first goods sold. Therefore, the ending inventory is assumed to contain the earliest purchases.

Notice that the cost of goods sold under LIFO is higher than that determined by the FIFO method. LIFO always results in a higher cost of goods sold when purchase costs are rising. Thus LIFO tends to minimize reported net income and income taxes during periods of rising prices in both perpetual and periodic systems.

Notice also that the LIFO method may result in an ending inventory that is priced well below its current replacement cost.

Receiving the Maximum Tax Benefit from the LIFO Method

Often, restating ending inventory using periodic costing procedures results in older (and lower) unit costs than those shown in the perpetual inventory records. When less cost is assigned to the ending inventory, it follows that more of these costs will be assigned to the cost of goods sold. A higher cost of goods sold, in turn, means lower taxable income.

Both the LIFO and average-cost methods produce different valuations of inventory under perpetual and periodic costing procedures. Only companies using LIFO, however, usually adjust their perpetual records to indicate the unit costs determined by periodic costing procedures. When FIFO is in use, the perpetual and periodic costing procedures result in the same valuation of inventory.

Pricing the Year-End Inventory by Computer

INTERNATIONAL FINANCIAL REPORTING STANDARDS

One major difference is that international standards do not recognize the LIFO method of accounting for the cost of inventory. Only the first-in, first-out (FIFO) or weighted average cost methods are acceptable under international standards. Remember that the conformity requirement under U.S. tax law requires a company that uses LIFO for tax purposes to also use that method in its financial statements.

Under U.S. generally accepted accounting standards, once an inventory is written down to a lower market value, recovery of that value before the inventory is sold is not permitted. Under international standards, however, the subsequent recovery of market value is treated as a reduction in cost of goods sold in the period of the recovery.

IMPORTANCE OF AN ACCURATE VALUATION OF INVENTORY

The most important liquid assets in the balance sheets of most companies are cash, accounts receivable, and inventory. Of these assets, inventory often is the largest. It also is the only one of these assets for which alternative valuation methods are acceptable.

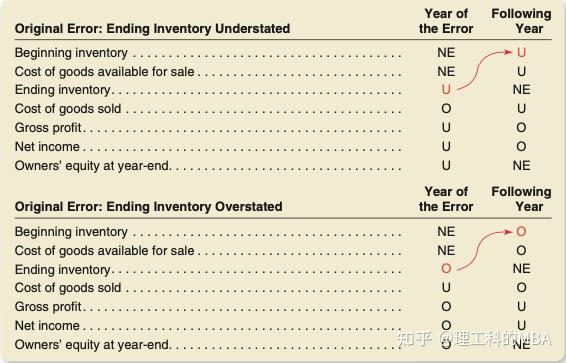

An error in the valuation of inventory will affect several balance sheet measurements, including assets and total owners' equity. It also will affect key figures in the income statement, including the cost of goods sold, gross profit, and net income. And remember that the ending inventory of one year is the beginning inventory of the next. Thus an error in inventory valuation will carry over into the financial statements of the following year.

Effects of an Error in Valuing Ending Inventory

To illustrate, assume that some items of merchandise in a company's inventory are overlooked during the year-end physical count. As a result of this error, the ending inventory will be understated. The costs of the uncounted merchandise erroneously will be transferred out of the Inventory account and included in the cost of goods sold. This overstatement of the cost of goods sold, in turn, results in an understatement of gross profit and net income.

Inventory Errors Affect Two Years

An error in the valuation of ending inventory affects not only the financial statements of the current year but also the income statement for the following year.

Notice that the original error has exactly the opposite effects on the net incomes of the two successive years.

The fact that offsetting errors occur in the financial statements of two successive years does not lessen the consequences of errors in inventory valuation. Rather, it exaggerates the misleading effects of the error on trends in the company's performance from one year to the next.

Effects of Errors in Inventory Valuation: A Summary

In Exhibit 8–9 we summarize the effects of an error in the valuation of ending inventory over two successive years. In this exhibit we indicate the effects of the error on various financial statement measurements using the code letters U (understated), O (overstated), and NE (no effect). The effects of errors in the valuation of inventory are the same regardless of whether the company uses a perpetual or a periodic inventory system. The NE for owners' equity at year-end in the Following Year column results from the offsetting of the first-year error in the second year.

TECHNIQUES FOR ESTIMATING THE COST OF GOODS SOLD AND THE ENDING INVENTORY

Therefore, if a business using a periodic inventory system prepares monthly or quarterly financial statements, it may estimate the amounts of its inventory and cost of goods sold except at the end of its annual period. One approach to making these estimates is called the gross profit method; another—used primarily by retail stores—is the retail method.

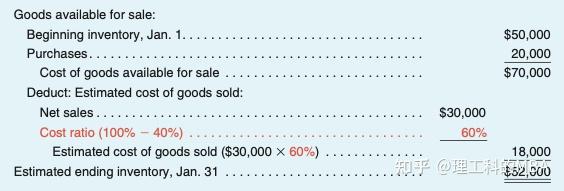

THE GROSS PROFIT METHOD

The gross profit method is a quick and simple technique for estimating the cost of goods sold and the amount of inventory on hand. Using this method assumes that the rate of gross profit earned in the preceding year (or several years) will remain the same for the current year. When we know the rate of gross profit, we can divide the dollar amount of net sales into two elements: (1) the gross profit and (2) the cost of goods sold.

When the gross profit rate is known, the ending inventory can be estimated by the following procedures:

- Determine the cost of goods available for sale from the general ledger records of beginning inventory and net purchases.

- Estimate the cost of goods sold by multiplying the net sales by the cost ratio.

- Deduct the estimated cost of goods sold from the cost of goods available for sale to find

the estimated ending inventory.

The gross profit method is also used at year-end after the taking of a physical inventory to confirm the overall reasonableness of the amount determined by the counting and pricing process. The gross profit method is not, however, a satisfactory substitute for periodically taking an actual physical inventory.

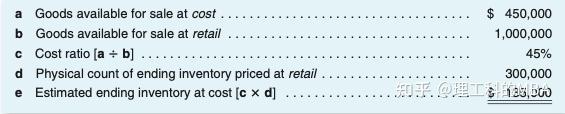

THE RETAIL METHOD

The retail method of estimating inventory and the cost of goods sold is similar to the gross profit method. The basic difference is that the retail method requires that management determine the value of ending inventory at retail prices. The retail value of ending inventory is then converted to its approximate cost using a cost ratio.

To determine the cost ratio, a business must keep track of goods available for sale at both cost and at retail prices.

This application of the retail method approximates a valuation of ending inventory at its average cost. A widely used variation of this method enables management to estimate a LIFO valuation of ending inventory.

"TEXTBOOK" INVENTORY SYSTEMS CAN BE MODIIED ... AND THEY OFTEN ARE

In practice, businesses often modify these systems to suit their particular needs. Some businesses also use different inventory systems for different purposes.

We described one modification in Chapter 6—a company that maintains little inventory may simply charge (debit) all purchases directly to the cost of goods sold. Another common modification is to maintain perpetual inventory records showing only the quantities of merchandise bought and sold, with no dollar amounts. Such systems require less record keeping than a full-blown perpetual system, and they still provide management with useful information about sales and inventories. To generate the dollar amounts needed in financial statements and tax returns, these companies might use the gross profit method, the retail method, or a periodic inventory system.

In summary, real-world inventory systems often differ from the illustrations in a textbook. But the underlying principles remain the same.

Source: https://zhuanlan.zhihu.com/p/438611110

0 Response to "The Inventory That Continually Discloses the Amount of Inventory on Hand is Called"

Post a Comment